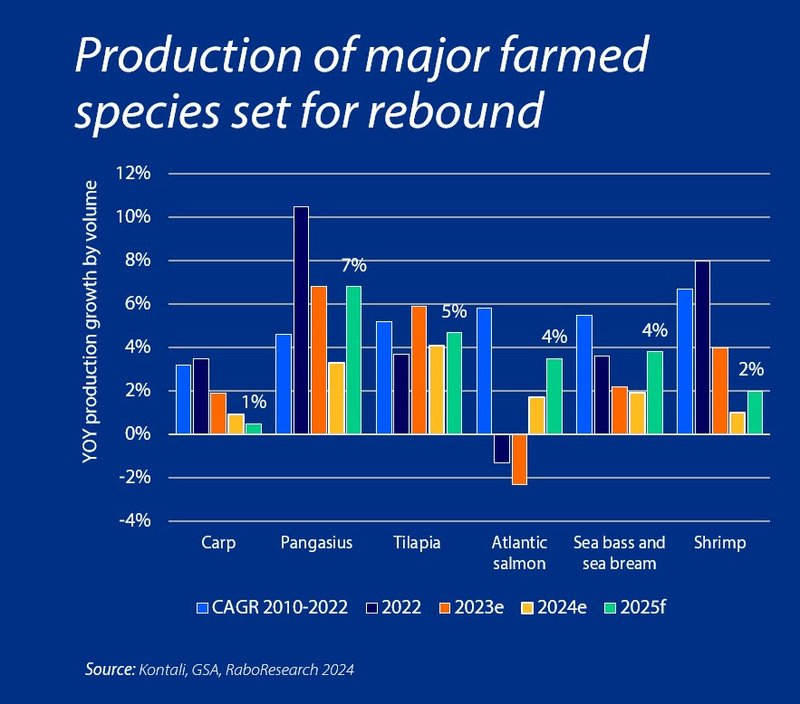

According to a new report from RaboResearch, the global aquaculture industry should see improved production growth for key species in 2025. Finfish production is poised to see the greatest growth, while shrimp, which continues to face relatively low prices, is expected to grow just 2% year-on-year. Lower feed prices and better demand should benefit producers. However, increasing tariffs and trade restrictions may impede the industry.

Salmon to return to growth in 2025

“Atlantic salmon production is expected to experience mild growth from 2024 to 2026, following two consecutive years of decline,” said Novel Sharma, Seafood analyst at RaboResearch. “Norway is poised to lead the growth, with year-on-year increases projected at 2.2% in 2025 and 5.3% in 2026, resulting in estimated outputs of 1.56 million and 1.64 million metric tons, respectively. This growth is contingent on stable biological conditions and improving harvest weights.”

After a difficult 2024, Chile is expected to gradually return to a growth trajectory, with a 1.4% year-on-year production increase expected in 2025 and 3.2% in 2026. However, production volumes are unlikely to surpass 2020 levels before 2026.

Shrimp production to remain slow amid ongoing low prices

“Despite relatively low prices, we expect global shrimp production growth will remain positive,” said Sharma. After years of strong growth, shrimp production is slowing, with volumes projected to increase by only 1% year-on-year in 2024 and 2% in 2025.

Latin America’s shrimp production is expected to slow, with growth rates dropping to 2% in 2024 due to lower prices. However, growth is anticipated to rebound to 4% in 2025 as the oversupply situation eases. Ecuador’s shrimp production, the world’s fastest-growing major aquaculture industry, will also experience a slowdown. China and India are poised for modest growth in 2025 – 1.7% and 2%, respectively. Meanwhile, Vietnam’s production is forecast to grow by 4% in 2025, although disease management and high production costs continue to pose challenges.

Pangasius and tilapia to see fastest production growth

Freshwater species are expected to have the highest growth among farmed species. Pangasius production is expected to grow robustly, up 7% year-on-year, with Vietnam leading the way, bolstered by rising demand from China. Global tilapia production is forecast to exceed 7 million metric tons, up 5% year-on-year, driven by strong growth in China and Indonesia.

Trade uncertainty ahead

According to RaboResearch’s annual aquaculture survey on finfish and shrimp production, performed in cooperation with the Global Seafood Alliance (GSA), the industry remains concerned about the market and economic conditions heading in 2025. Ongoing geopolitical uncertainties pose significant challenges.

“Seafood is the most traded animal protein, with a larger trade value than all other animal proteins combined,” explained Sharma. “Donald Trump’s presidential victory in the US could mean new import tariffs. This is especially significant for the seafood sector, as the US is the world’s largest importer, relying on imports for over 80% of its seafood consumption. Moreover, the potential trade war is likely to involve China, the world’s largest seafood producer, exporter, and re-processor.”

Market prices a key industry concern

According to survey results, market prices are once again the top industry concern heading into the coming year, followed by aqua feed costs and market access. “This is understandable,” said Sharma. “2024 had some of the lowest seafood prices we have seen in many years. Although demand has started to improve for many species, prices are increasing from a low point, and the improvement is tentative. Possible trade restrictions from the US and the uncertain recovery of Chinese, Japanese, and European import demand in 2025 are clear concerns.”